General Principles

Policy Preferences

We will participate in our political, legislative and regulatory processes in an ethical and forthright manner, advocating for policies that benefit our company, our employees, our industry and the communities we serve.

Competitive Markets

We believe in the power of competition to spark innovation and unleash customer benefits and value. As such, we believe that markets should be allowed to function freely with minimal oversight and regulated only to the extent needed to ensure a fair and equitable treatment of market participants and customers.

Out of Market Subsidies

We believe that the competitive market works best without outside interference. Out-of-market subsidies run counter to a well-functioning competitive electricity market. We recognize, however, that it is not always possible to avoid subsidies for various policy or political reasons. Therefore, should subsidies be implemented, we believe that such subsidies should be targeted, technology neutral, time limited and phased out as the rationale for the subsidized item becomes obsolete

Traditional Generation

We believe that coal, natural gas, nuclear and other “traditional” electric generation facilities continue to have a role to play in generating safe, reliable and secure power to customers. We believe these facilities operate best in competitive markets as part of a broad generation portfolio.

Alternative Generation

We understand that the generation methods of today will not always be the generation methods of tomorrow. We believe in pursuing economic and appropriate opportunities to integrate new generation technologies and approaches into the grid. We further believe that in competitive areas, such technologies or approaches should be backed by private investment and not subject to market distorting mandates or public subsidization.

Customer Protections

We believe that customers should be protected against bad actors in the market. As such, we believe that customer protection regulations should provide relief to customers in these situations. We believe that customer protections should be structured in such a way that does not inhibit innovation, prevent fair business practices or punish good actors operating in good faith.

Low-Income & Vulnerable Group Protections

We believe that certain groups of customers may require greater assistance and/or protections than other classes. Among these are low-income, elderly, and medical critical care customers. We support public and private programs to assist these customers with their electric needs and protections to ensure they have the electricity they need to prevent life-threatening conditions.

Taxation

We support paying our fair share of taxes. We believe the levy of taxes should be equitable, understand the value characteristics of electric generation, and shouldn’t favor one taxpaying group over another.

Cybersecurity

We believe in operating in a safe and secure manner. We believe security is increased through knowledge sharing amongst private and public parties and by the publication of standard frameworks created with stakeholder input. We believe that security is better served with one-national standard rather than a patch-work of standards across jurisdictions. We further believe that companies operating in good faith and in compliance with established standards, best practices and frameworks should have limited liability as the victim of a successful cyberattack.

Environment

We believe in operating our company and facilities in a clean and environmentally friendly manner. As such, we will always comply with existing environmental regulations. We further believe that any new environmental laws and regulations should be targeted, based on sound science, and that their costs be commensurate with the benefits obtained. Environmental reporting should be based on actual measured data, consolidated as much as possible and should not create an undue compliance burden.

EV & EV Infrastructure

Vistra supports the adoption of electric vehicles and the build out of EV infrastructure, including charging stations. Vistra believes that EVs and EV infrastructure are competitive products and should be provided through the competitive market. While Vistra does not support subsidization of competitive products in general, if legislative or regulatory action is taken to provide out-of-market support to EVs or EV infrastructure Vistra believes that these out-of-market actions should be targeted, time limited and done outside of utility rates.

Its About Choice.

Bottom line, competition is about giving customers choice. It means recognizing that consumers make choices on more than one variable. It recognizes that every consumer is different and that one-size-fits-all approaches to markets do not afford the best combination of value, innovation or satisfaction.

Retail electric competition allows price conscious consumers to select the lowest cost offer in the market. For customers who value 100% green energy, competition enables them to purchase plans that match their preferences. For consumers who are more internet savvy, they can have the choice to select offers with discounts for internet only customer service. Likewise, consumers who prefer to have a person to talk to 24-7-365, can find plans that cater to those needs. For some customers, the peace of mind of locking in a fixed rate contract, allowing them to avoid future price volatility, is worth potential price premiums if prices go lower and allows them to better budget their energy costs.

In the end, it’s not about just price, it’s about letting consumers decide for themselves what the best balance is between affordability, service, environmental consciousness and other factors to best fit their needs.

Customer Protections

Customer Protections

Competitive markets naturally force competitors to focus on the customer. Those companies who are unable to provide value to their customers or treat their customers like commodities instead of valued partners are appropriately forced out of the market through market dynamics. Even so, there are unfortunately always companies that behave unethically or illegally to the detriment of the market and consumers. Vistra believes that customers should be protected against bad actors in the market. Customer protection regulations should provide relief to customers who have been negatively impacted by these bad actors and work to prevent bad actors from entering or remaining in the market. Customer protections should be structured in such a way that does not inhibit innovation, prevent fair business practices or punish good actors operating in good faith.

A Market Leader in Low-Income & Vulnerable Group Protections

Whether it’s keeping customers cool from the heat of summer, warm in the depths of winter, or powering critical home medical equipment, electricity can be a life-preserving necessity rather than just a modern convenience. Vistra understands that certain groups of customers may require greater assistance and/or protections than other groups. Among these are low-income, elderly, and medical critical care customers. Our company works with numerous federal, state, and local officials and advocacy groups to spread awareness about energy assistance and energy efficiency programs. Through our support of public and private programs to assist these at-risk customers with their electric needs we help ensure they have the electricity they need to prevent life-threatening conditions.

For example, in Texas, our retail brand implemented summer customer protections that went beyond what was required by law. In four consecutive years (2007-2010), TXU Energy implemented a voluntary moratorium on disconnects for customers designated as low-income, ill or disabled, or who were at least 62 years of age, as well as providing more flexible deferred payment plans for these customers. The company was publicly recognized for our summer protections by key community leaders, PUC Commissioners and state legislators, among others. Starting in the summer of 2011, the Texas PUC implemented a rule which was very similar to TXU Energy’s voluntary program. The rule mandated that all Texas retail electric providers implement a moratorium on summer disconnections to help the most vulnerable during the hot Texas summer.

Additionally, for over 35 years, customers of our TXU Energy brand in Texas have been able to take advantage of one-time bill payment assistance through our TXU Energy AidSM program, which is one of the largest privately funded electric bill payment assistance programs in the U.S. This assistance is in addition to any aid customers can receive through state, federal and other programs. Customer assistance such as this, paired with appropriate customer protections, helps to ensure that customers never have to choose between affording their electricity and avoiding life-threatening conditions.

Fisher, Sheehan & Colton Affordability Gap Studies

In an effort to quantify the gap between “affordable” home energy bills1 and “actual” home energy bills, Fisher, Sheehan & Colton (FSC) (a firm specializing in poverty law and economics) developed a model that estimates the “home energy affordability gap” on a county-by-county basis for the entire country. Introduced in April 2003 (using 2002 energy prices), the initial FSC Home Energy Affordability Gap analysis found that the annual “affordability gap” reached roughly $18.2 billion and that federal fuel assistance provided through the Low-Income Home Energy Assistance Program (LIHEAP) covered just a fraction of that gap. Updates of the Home Energy Affordability Gap have been published annually.

The 2017 Home Energy Affordability Gap, published in April 2018, continues the 2nd Series of FSC’s annual Affordability Gap analysis begun in 2012.2 The following matrix provides FSC’s findings from their 2018 analysis (using 2017 data):

| Region | Gap 2011 (Base Year, Millions) | Gap 2017 (Current Year, Millions) | Index3 | LIHEAP Allocation (Thousands) | # Households < 150% Fed. Poverty Level | LIHEAP Covered Heat / Cool Bills |

| Total US | $ 38,577.6 | $ 47,648.6 | 123.4 | $ 2,960,952 | 28,761,009 | 3,224,511 |

| California | $ 2,217.9 | $ 3,295.9 | 148.6 | $ 151,804 | 3,283,627 | 329,294 |

| Connecticut | $ 659.7 | $ 449.0 | 68.1 | $ 70,021 | 226,524 | 59,898 |

| Illinois | $ 1,340.8 | $ 2,216.9 | 165.3 | $ 148,385 | 1,092,303 | 118,235 |

| Maine | $ 471.0 | $ 269.9 | 57.3 | $ 33,462 | 126,523 | 23,799 |

| Massachusetts | $ 1,096.3 | $ 658.2 | 60.0 | $ 130,772 | 460,564 | 136,934 |

| New Jersey | $ 9633 | $438.3 | 45.5 | $ 106,604 | 561,892 | 157,698 |

| New York | $ 4,100,2 | $ 2,198.5 | 53.6 | $ 324,884 | 1,763,224 | 403,583 |

| Ohio | $ 1,623.0 | $ 1,439.3 | 88.7 | $ 131,268 | 1,122,872 | 134,084 |

| Pennsylvania | $ 1,872.2 | $ 1,249.7 | 66.7 | $ 185,523 | 1,073,629 | 197,786 |

| Texas | $ 3,553.4 | $ 3,418.5 | 96.2 | $ 104,972 | 2,511,935 | 113,606 |

| Virginia | $ 921.4 | $ 1,816.5 | 197.1 | $ 74,449 | 599,076 | 53,368 |

| W. Virginia | $ 312.2 | $ 319.9 | 102.5 | $ 25,849 | 212,153 | 26,511 |

[1] The “affordable burden” for home energy bills is set at 6% of gross household income for the Home Energy Affordability Gap model. This burden takes into account the total cost of shelter and the proportion of total shelter cost devoted specifically to energy. The “affordable burden” for home heating and cooling is set at 2% of gross household income.

[2] While the energy affordability gap includes more than just electricity, it is an instructive measure to help show the gap between need and available assistance. Data sets and additional information can be found at the FS&C website: http://www.homeenergyaffordabilitygap.com/03a_affordabilityData.html (last accessed 08/14/18).

[3] The home Energy Affordability Gap Index (2nd Series) uses the year 2011 as its base year. The Index for 2011 is set equal to 100. A current year Index of more than 100 thus indicates that the Home Energy Affordability Gap has increased since 2011. A current year Index of less than 100 indicates that the Home Energy Affordability Gap has decreased since 2011.

Low-Income Support

Alternative Generation and Storage

Alternative Generation

In the competitive market, Vistra understands that the generation methods of today will not always be the generation methods of tomorrow. We believe in pursuing economic and appropriate opportunities to integrate new generation technologies (wind, solar, storage, etc.) and approaches (microgrids, distributed generation, etc.) into the grid. We further believe that in competitive areas, such technologies or approaches should be backed by private investment and not subject to market distorting mandates or public subsidization.

Vistra will invest strategically in alternative energy resources and storage opportunities as they become economic and provide competitive opportunities. Our investments to date demonstrate that alternative generation and storage go beyond just “being green”.

Retail Products that Leverage Renewable Opportunities

Competitive retail markets provide increasing opportunities for retail electric companies to leverage renewable generation existing in the market. Beyond the increasing interest by customers (both residential and commercial) of being “green” and sustainable in their energy consumption, retailers are able to provide innovative plans to differentiate themselves in the market and meet consumer preferences.

For example, in ERCOT, Vistra is already in the behind-the-meter solar business by providing customers electricity plans with solar energy in them. Our Texas retail arm has launched four solar plans since 2016, including our community solar offer “SolarClub”, which allows customers to invest in solar energy without the cost or expense of installing solar panels at their residence and our ”Free Nights and Solar Days”, which allows customers to power their homes with off-site solar during the day and take advantage of low-cost wind resources at night. These plans have been highly popular, signing up more customers than all Solar Photovoltaic Rooftops in ERCOT combined. This is an example of Vistra’s integrated model at work – offering innovative renewable products to end use consumers by leveraging generation from our own utility scale solar farm and access to other facilities.

Vistra has also invested in rooftop solar, launching our TXU Solar from SunPower in 2015. While penetration of rooftop solar is low due to challenged economics, we see rooftop solar continuing to increase in adoption, especially as home energy storage becomes more affordable. Our retail brand also offers “net-metering” to customers with installed solar photovoltaic, regardless of whether the solar photovoltaic system was installed through our own offer or via another provider.

Vista Energy’s experience isn’t limited to residential customers. We are able to bring our experience in the wholesale market and renewable products to help commercial customers of all sizes meet their renewable and sustainable energy goals. Regardless of whether the customer is a small family or a large data storage facility, Vistra plans to continue to innovate in this space and bring the increasing value that these type of offerings provide to our customers.

Large Scale Renewable Generation & Storage

Vistra is able to offer innovative renewable retail products, in part, due to our investments in renewable energy and storage at the wholesale level.

In June 2018, Vistra announced that its Upton 2 Solar Power Plant in West Texas achieved commercial operations. Capable of generating 180 MW of electricity, Upton 2 is the largest operating solar facility in Texas. The site sits on nearly 1,900 acres (roughly the size of 1,424 football fields) and consists of 718,000 photovotaic panels. The generation capacity of the facility is enough to power approximately 56,700 residences in ERCOT during normal weather conditions and about 27,700 during peak conditions. Vistra purchased Upton 2 in May 2017 while the site was still under development because it provided a perfect fit for the company’s integrated business model. It not only enabled the company to enhance its retail solar offerings but also helped diversify the company’s generation fleet.

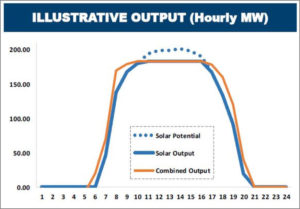

At Vistra’s Analyst Day in June 2018, the company announced the coupling of battery storage with the Upton 2 solar generation, targeted for the fourth quarter of 2018. The storage will be a 10 MW / 42 MWh lithium ion battery and will provide several advantages to the solar facility. First and foremost, it will enable any excess energy generated to be beneficially stored for later use. Although the facility is rated for 180 MW, it has the capability to generate more than that amount. In these cases, if the storage was not available, that excess energy would be “clipped” as the grid would only accept up to the rated 180 MW amount. With storage, these times of excess generation can be captured and time-shifted to other periods. Secondly, this time shifting nature allows the facility to provide peak output for more hours of the day than solar alone. This provides “wider shoulders” during peak solar power production, along with more consistent, predictable and slightly extended ramp-up and ramp-down periods (see graphic below).

Vistra’s investments are not limited to just Texas. Though we started in Texas, the company’s recent merger with Dynegy has opened up opportunities in other markets. One such example is the development of battery storage at one of Dynegy’s natural gas generation facilities in California. Also in June 2018, the company announced that it planned to enter a 20-year resource adequacy contract with Pacific Gas and Electric Company (PG&E). Under the contract, Vistra will develop a 300 MW/1,200 MWh, battery energy storage project at its Moss Landing Power Plant site in Moss Landing, California. The Moss Landing battery project will be the largest of its kind in the world and will position Vistra as a market leader in utility-scale battery development. This project is consistent with Vistra’s strategy to opportunistically invest in new technologies in support of the changing energy supply landscape.

The Moss Landing example shows how existing infrastructure can be leveraged in new ways to facilitate emerging technologies. The battery project will leverage the existing interconnection, reducing regulatory hurdles, and will be able to leverage existing development on the site, reducing construction costs. Pending approval by the California Public Utilities Commission, Vistra anticipates the battery storage project will enter commercial operations by the fourth quarter of 2020.

The Market for Renewables & Storage

Vistra is making these investments because the market for renewable and storage products is growing. There are a broad range of market drivers, both commercial and political, that are setting the pace of growth in the renewable and storage space, and that pace is accelerating.

Corporate procurement of renewables is virtually a universal trend. Advanced Energy Economy reports that 215 Fortune 500 companies (43 percent) have a sustainability target, a renewable energy target, or both. However, corporate interest in green power isn’t limited to large enterprises. Internationally, an array of small- and mid-cap companies is also procuring renewable energy and setting ambitious carbon reduction goals. There are several reasons why companies of all sizes are taking a keen interest in procuring renewable energy. As one might expect, economics are a significant driver. Solar and wind power are now cost-competitive with electricity generated from fossil fuels in many areas of the world. Furthermore, the predictable, rather than fluctuating, costs of renewables can provide a hedge against future fuel price volatility. But there are other forces at work as well. Businesses are setting sustainability goals to enhance their reputations and satisfy their investors and customers, who are increasingly demanding action on environmental stewardship and climate change. While this factor is harder to quantify, more and more companies around the world appear to be embracing the concept that being a good corporate citizen is good business and helping to “green the grid” is an important part of that equation.1

Renewable energy has become serious business for corporate buyers, to the extent that many corporate buyers are uniting under a trade group and publishing a set of principles to encourage and simplify access to renewable energy:

- Greater choice in procurement options

- More access to cost-competitive options

- Longer and variable-term contracts

- Access to new projects that reduce emissions beyond business as usual

- Streamlined third-party financing

- Increased purchasing options with utilities

At Vistra, we believe the majority (if not all) of these principles can be met through functioning competitive markets at the retail and wholesale level. However, not all markets are created equal and there are variables to consider in each market for the deployment of renewable and storage facilities.

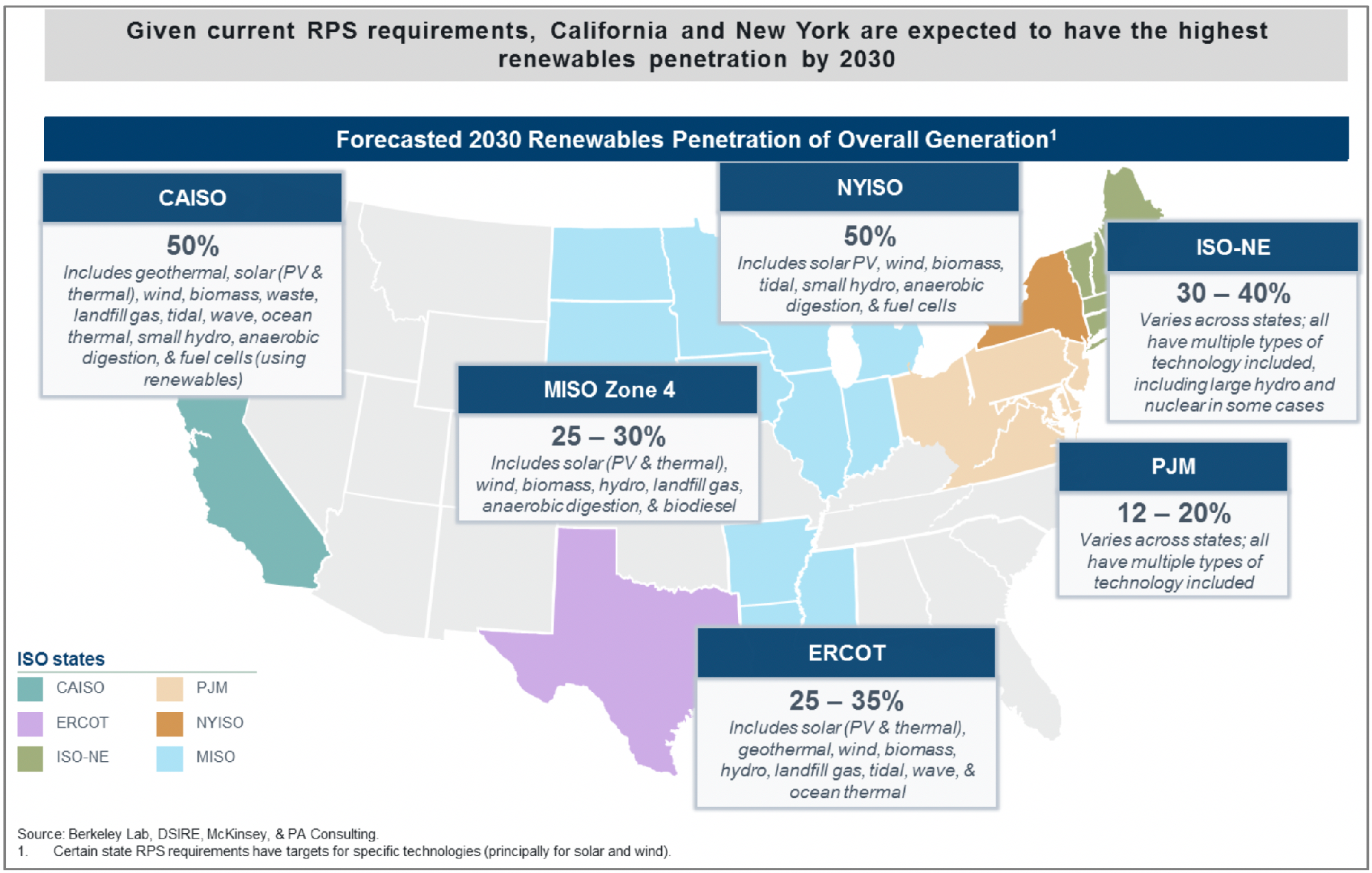

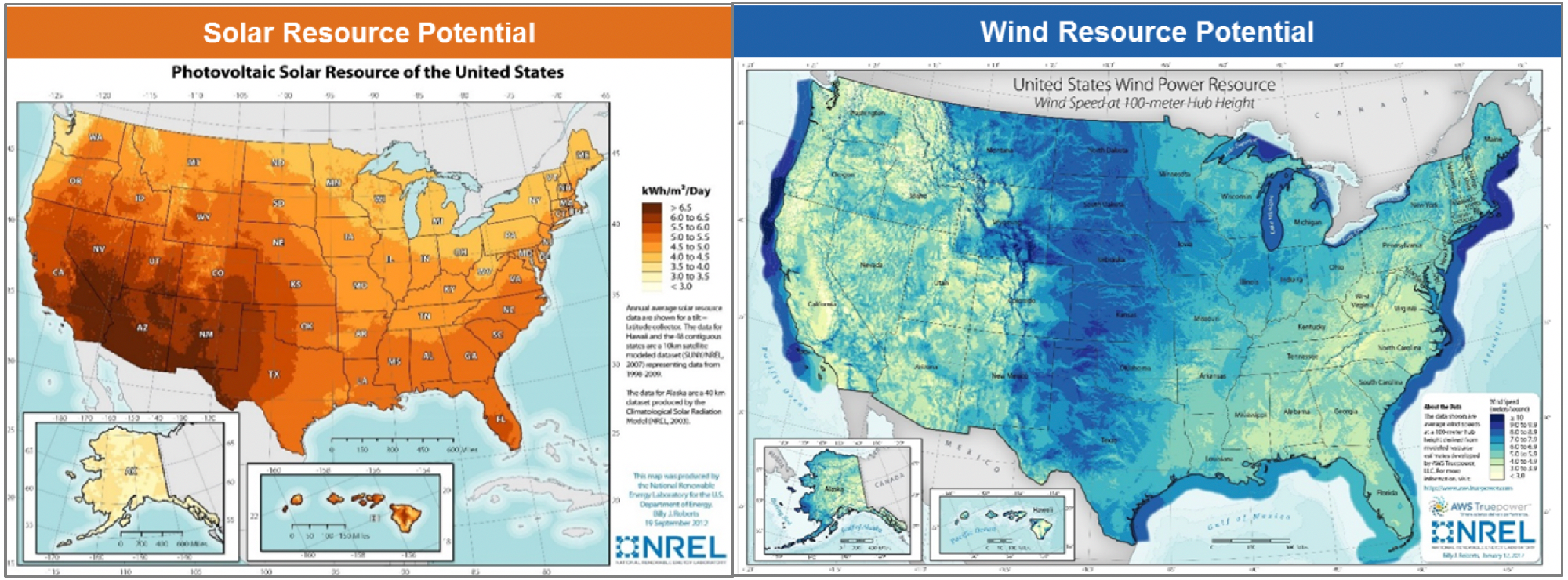

Most areas with high solar and wind resource potential in the U.S. are located far from population centers, and the PJM2 and ISO-NE3 regions have relatively low resource potential for both wind and solar. In areas with low resource potential, RPS4 requirements are more likely to drive renewable development, whereas economics are more likely to drive requirements in areas with high resource potential. RPS policies have driven 70-90% of the growth in renewables in the West, Mid-Atlantic, and Northeast, but in Texas and the Midwest, growth has far outstripped RPS requirements, largely due to attractive wind economics (see graphics below). 5

Despite RPS subsidies in Mid-Atlantic and Northeast states, the impact on capacity and energy markets is materially reduced due to mitigation measures and resource effectiveness; in addition, some states have broadened the definition of renewables to meet RPS targets (e.g., large scale hydro)

[1] “Serious Business: Corporate Procurement Rivals Policy in Driving Growth of Renewable Energy”, Deloitte Center for Energy Solutions. 2017

[2] PJM Interconnection coordinates the movement of electricity through all or parts of Delaware, Illinois, Indiana, Kentucky, Maryland, Michigan, New Jersey, North Carolina, Ohio, Pennsylvania, Tennessee, Virginia, West Virginia and the District of Columbia.

[3] ISO New England (ISO-NE) Interconnection coordinates the movement of electricity through all or parts of Connecticut, Rhode Island, Massachusetts, Vermont, New Hampshire, and Maine.

[4] Renewable Portfolio Standards (RPS) require utilities to ensure that a percentage, or a specified amount, of the electricity they sell comes from renewable resources. States have created these standards to diversify their energy resources, promote domestic energy production and encourage economic development. Roughly half of the growth in U.S. renewable energy generation since 2000 can be attributed to state renewable energy requirements. Additional information is available at NCSL website: http://www.ncsl.org/research/energy/renewable-portfolio-standards.aspx.

[5] “Supercharged: Challenges and Opportunities in Global Battery Storage Markets”, Deloitte Center for Energy Solutions. 2018

The Case for Energy Storage

Battery storage is flexible, can be deployed quickly, has multiple applications, and can produce numerous value streams—not to mention that battery prices are falling faster than anticipated. However, the dynamism in the sector is not solely attributable to these factors. Advances in adjacent digital technologies, such as artificial intelligence, blockchain, and predictive analytics, are giving rise to aggregated solutions and innovative business models that were nearly inconceivable a few years ago. Start-ups around the world are rapidly commercializing intelligent networks of “behind-the-meter” batteries to benefit electricity customers, utilities, and grid operators.[1]

Although research and market dynamics have shown increases in company procurement of renewable energy, there are those that have indicated they are not working to procure more renewable energy. However, amongst those companies a survey has found that a solid majority (58 percent) said combining renewables with battery storage would motivate them to do more. This concept particularly appealed to small companies (63 percent). This could potentially be due to the desire of small companies, which are presumably on tight budgets, to avoid demand charges. Battery storage could help by giving more operational flexibility.[2]

As already mentioned, Vistra sees a growing market in coupling energy storage with both renewable and traditional generation facilities. The value chain of deploying energy storage in this way extends from the generation facilities, to the grid, to the end use customer themselves. For example, batteries are often supportive of existing generation where daily cycle requires charging on a day-to-day basis. Furthermore, baseload coal, nuclear, and low-cost gas plants can benefit to the extent that energy storage:

- Charges overnight and can raise off-peak prices; and

- Smooths / eliminates extremely low-priced hours from high renewable penetration.

Near term, energy storage is most likely to threaten investment in new peaking plants where short duration storage may allow existing peaking plants to provide non-spinning reserves[3] (instant start). In these cases, storage can help normalize existing markets from distortive effects and at the same time potentially reduce future costs to consumers by delaying the cost of new build.

Furthermore, energy storage deployment is not something that has to be a “rate base” investment even in traditional utility territories. Vistra, and companies like ours, can contract with traditional utilities to provide reliability services from battery projects. This way, the value of the batteries can be maximized because the batteries would provide the traditional utilities with electricity transmission and distribution related reliability services while also being able to provide energy and ancillary services. Utilities could conduct competitive bidding processes for the services they require and then the competitive company would be able to optimize other services from the batteries.

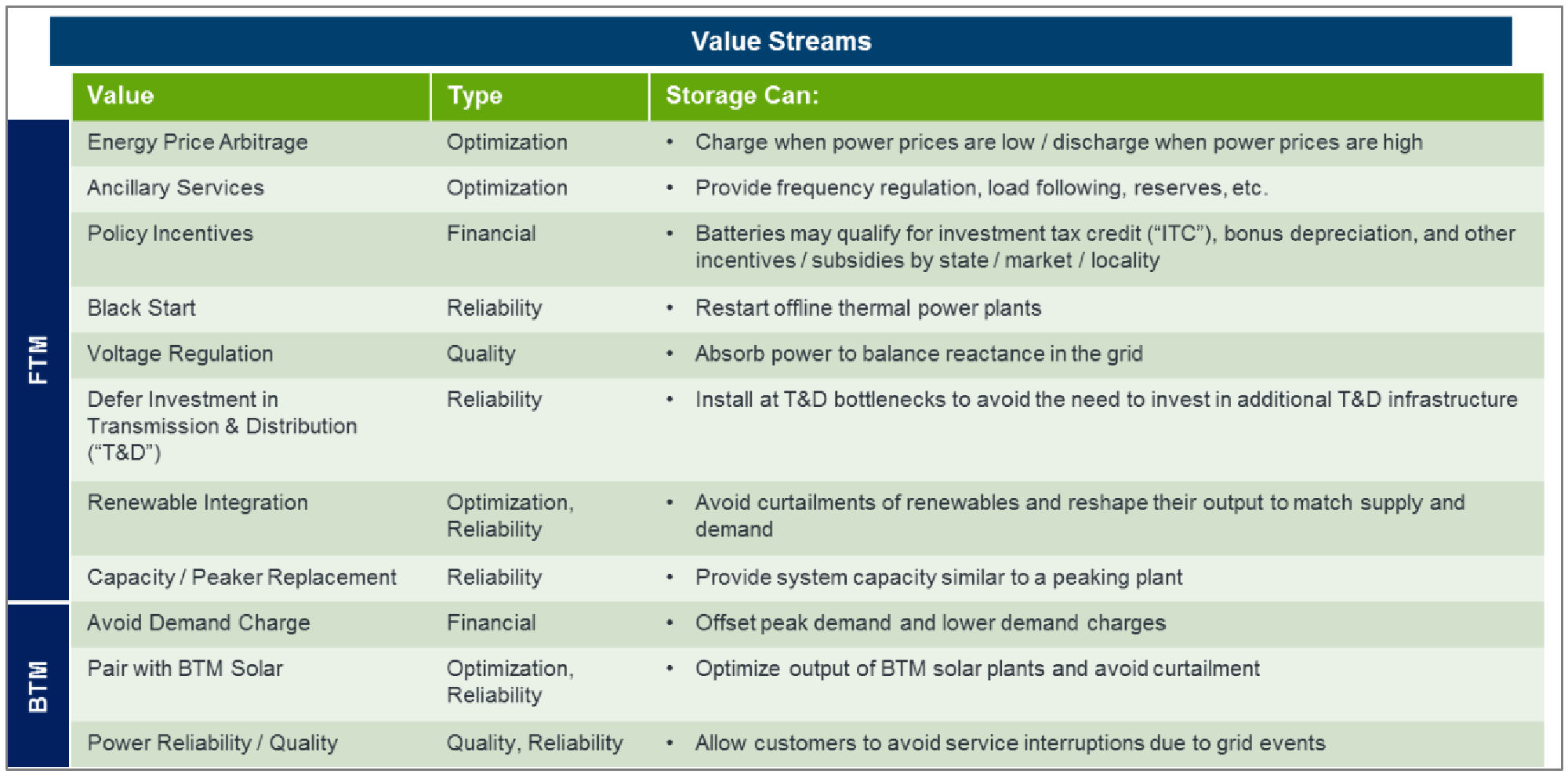

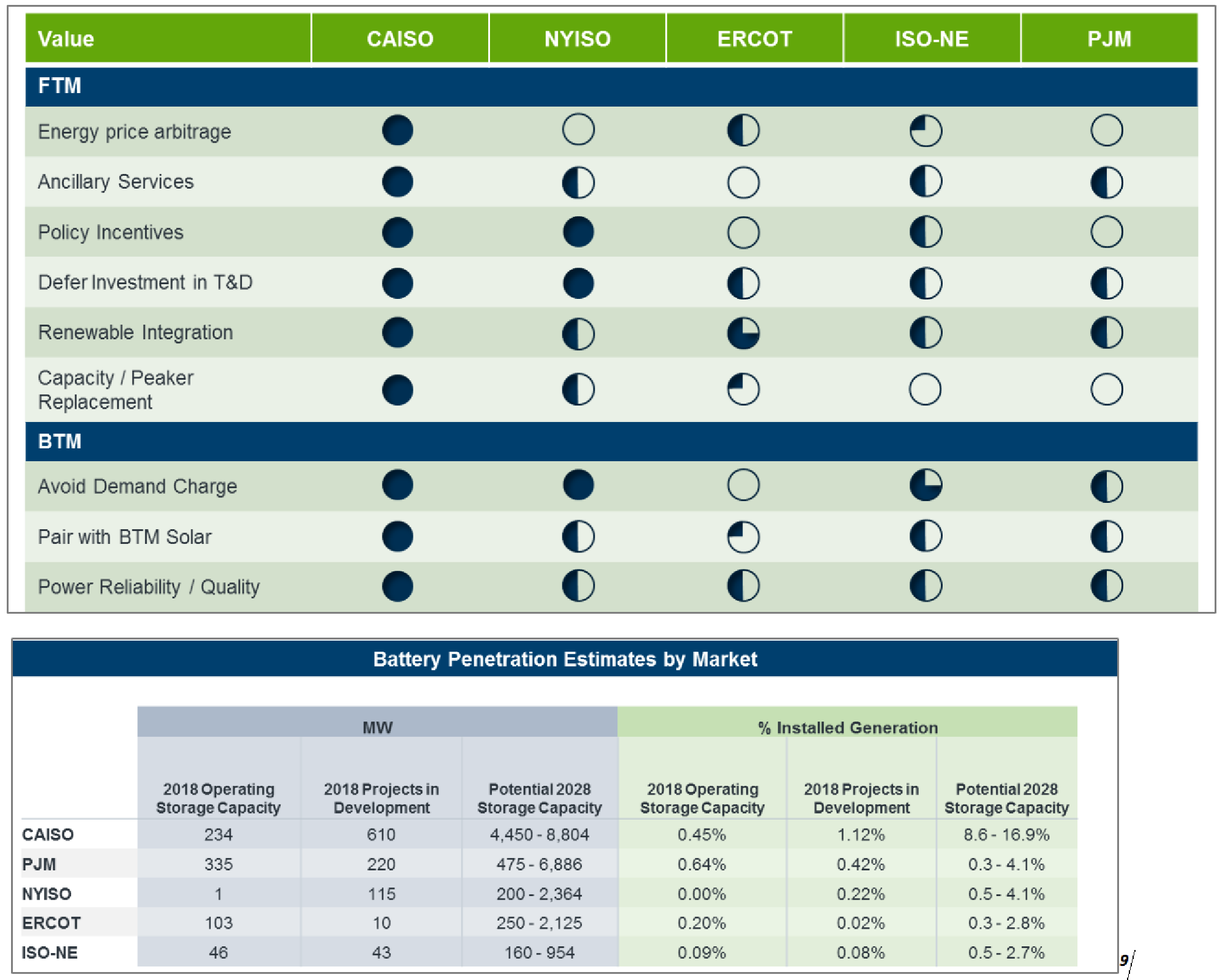

Front of the meter (FTM) services, such as the examples above, are not the only area where energy storage brings value. Behind the meter (BTM) is where the customer most directly sees the value of energy storage. This can include better power quality / reliability, pairing with distributed energy generation, microgrids, or demand shaving (helping to reduce demand charges). In the end, multiple value streams contribute to energy storage economics for both FTM and BTM applications (see graphic).

As with renewable generation, we believe the competitive market provides the best venue for realizing the value of energy storage. However, as previously stated, not all markets are equally well suited for competitive energy storage deployment. The graphic below shows Vistra’s perspective on the viability and deployment of energy storage amongst the five different markets we compete in, California being the most attractive market, followed by New York:

[1] “Supercharged: Challenges and Opportunities in Global Battery Storage Markets”, Deloitte Center for Energy Solutions. 2018

[1] “Supercharged: Challenges and Opportunities in Global Battery Storage Markets”, Deloitte Center for Energy Solutions. 2018

[2] “Serious Business: Corporate Procurement Rivals Policy in Driving Growth of Renewable Energy”, Deloitte Center for Energy Solutions. 2017

[3] Operating reserve, which is made up of the spinning reserve as well as the non-spinning or supplemental reserve, is the generating capacity available to the system operator within a short interval of time to meet demand in case of a disruption to the supply. The non-spinning reserve or supplemental reserve is the reserve that is not currently connected to the system but can be brought online after a short delay. This could be generation available from fast-start generators within the region, importing power from other regions, or retracting power that is currently being exported to other regions. The spinning reserve is the extra generating capacity that is available by increasing the power output of generators that are already generating electricity and have capacity to generate more.

Beyond the Grid: Electrification of Transport

Battery storage is flexible, can be deployed quickly, has multiple applications, and can produce numerous value streams—not to mention that battery prices are falling faster than anticipated. However, the dynamism in the sector is not solely attributable to these factors. Advances in adjacent digital technologies, such as artificial intelligence, blockchain, and predictive analytics, are giving rise to aggregated solutions and innovative business models that were nearly inconceivable a few years ago. Start-ups around the world are rapidly commercializing intelligent networks of “behind-the-meter” batteries to benefit electricity customers, utilities, and grid operators.[1]

Although research and market dynamics have shown increases in company procurement of renewable energy, there are those that have indicated they are not working to procure more renewable energy. However, amongst those companies a survey has found that a solid majority (58 percent) said combining renewables with battery storage would motivate them to do more. This concept particularly appealed to small companies (63 percent). This could potentially be due to the desire of small companies, which are presumably on tight budgets, to avoid demand charges. Battery storage could help by giving more operational flexibility.[2]

As already mentioned, Vistra sees a growing market in coupling energy storage with both renewable and traditional generation facilities. The value chain of deploying energy storage in this way extends from the generation facilities, to the grid, to the end use customer themselves. For example, batteries are often supportive of existing generation where daily cycle requires charging on a day-to-day basis. Furthermore, baseload coal, nuclear, and low-cost gas plants can benefit to the extent that energy storage:

- Charges overnight and can raise off-peak prices; and

- Smooths / eliminates extremely low-priced hours from high renewable penetration.

Near term, energy storage is most likely to threaten investment in new peaking plants where short duration storage may allow existing peaking plants to provide non-spinning reserves[3] (instant start). In these cases, storage can help normalize existing markets from distortive effects and at the same time potentially reduce future costs to consumers by delaying the cost of new build.

Furthermore, energy storage deployment is not something that has to be a “rate base” investment even in traditional utility territories. Vistra, and companies like ours, can contract with traditional utilities to provide reliability services from battery projects. This way, the value of the batteries can be maximized because the batteries would provide the traditional utilities with electricity transmission and distribution related reliability services while also being able to provide energy and ancillary services. Utilities could conduct competitive bidding processes for the services they require and then the competitive company would be able to optimize other services from the batteries.

Front of the meter (FTM) services, such as the examples above, are not the only area where energy storage brings value. Behind the meter (BTM) is where the customer most directly sees the value of energy storage. This can include better power quality / reliability, pairing with distributed energy generation, microgrids, or demand shaving (helping to reduce demand charges). In the end, multiple value streams contribute to energy storage economics for both FTM and BTM applications (see graphic).

As with renewable generation, we believe the competitive market provides the best venue for realizing the value of energy storage. However, as previously stated, not all markets are equally well suited for competitive energy storage deployment. The graphic below shows Vistra’s perspective on the viability and deployment of energy storage amongst the five different markets we compete in, California being the most attractive market, followed by New York:

[1] “Supercharged: Challenges and Opportunities in Global Battery Storage Markets”, Deloitte Center for Energy Solutions. 2018

[2] “Serious Business: Corporate Procurement Rivals Policy in Driving Growth of Renewable Energy”, Deloitte Center for Energy Solutions. 2017

Reductions in battery storage costs are increasing attractiveness of electric vehicles (EVs). EVs, ride-sharing, and automation is a virtuous cycle that we see playing out over the next ~10-15 years. Battery advancement will impact EVs through improvements in battery storage costs, duration, and energy density, which have improved storage economics on the wholesale side, are making EVs more competitive. Over the next ~5 years, EVs as a source of power demand will offset some of the demand reductions from demand response and energy efficiency. In the ~10-15 years, EVs may end up representing a significant source of power demand growth

EV penetration will likely be confined primarily to metropolitan areas, particularly on the coasts. Continued EV penetration will be affected by low gas prices and easing fuel economy regulations, availability of charging infrastructure, improvements to driving range and increased model availability/affordability.

The proliferation of EVs may also help with air quality and greenhouse gas emissions (GHGs). Currently, the transportation and power sectors are the leading sources of greenhouse gas (“GHG”) emissions in the United States. However, in 2016, the transportation sector overtook the power sector as the largest contributor of GHG emissions. This was driven in part by coal-gas switching and an increase in renewables generation. It is estimated that for each EV that replaces an internal combustion engine vehicle there will be a 3x savings in GHG emissions.

Out-of-Market Subsidies

Markets Function Best with Minimal Interference

Vistra believes that the competitive market works best without outside interference. As stated in an open letter to policymakers by eight leading economists:

Among economists, it is almost universally accepted that well-functioning competitive electricity markets yield the greatest benefits to consumers in terms of price, investment and innovation especially when regulated alternatives are no longer warranted[1]

As such, Vistra opposes direct out-of-market subsidies as they run counter to a well-functioning competitive electricity market. Out-of-market subsidies, no matter how well intentioned, tend to have market distortive effects and unintended consequences. Vistra recognizes, however, that it is not always possible to avoid implementing subsidies for various policy or political reasons. Therefore, should subsidies be implemented, Vistra believes that such subsidies should be targeted, technology neutral, time limited and phased out as the rationale for the subsidized item becomes obsolete.

[1] Joskow, Paul L.; Kahn, Alfred E.; et al., “An Open Letter to Policymakers”, June 26, 2006 (last accessed 8/23/18).

The Changing Nature of Generation Economics

As has occurred with many other industries, the electric generation industry is undergoing a seismic market change. For decades, electric generation was based on a centralized model focused on a few large electric generation facilities that ran continuously and were powered mostly by fossil fuels. These plants provided a “baseload” level of electric generation and were supplemented by generation facilities that could quickly ramp up and down as the need for electricity fluctuated. Economically, the baseload plants were often the cheapest sources of electricity, and thus dispatched to serve load continuously. The supplemental facilities were generally more expensive and were dispatched only as needed. Since the supplemental facilities were dispatched only as needed, they often set the cost of electricity in a market.

In the mid-2000s, this model of electric generation began to change. The cost-effective ability to “frack” natural gas resources significantly lowered natural gas prices, which in turn significantly lowered wholesale electric prices. Baseload coal and nuclear generation facilities were no longer necessarily the cheapest fuel to produce electricity in a region. Additionally, increasing deployment of renewables also impacted prices. With almost no marginal costs and the benefit of state renewable portfolio targets as well as federal subsidies, renewables also put downward pressure on electric wholesale prices.

The resulting lower generation costs for natural gas and renewable facilities coupled with lower wholesale electric market prices resulted in two key changes to electric markets. First, using economic dispatch models, renewable energy and natural gas generation facilities became the most cost-effective means to generate electricity in many regions. This shifted the dispatch curve, meaning many previous baseload generation facilities were no longer as cost-effective to dispatch and, therefore, ran less often, impacting their revenues. Secondly, lower overall wholesale market prices for electricity meant that those facilities that were dispatched were paid less for each unit of electricity they produced. While this has created situations where new build is not cost-effective in many regions, it has also created a situation where many existing legacy baseload generation facilities (mainly coal and nuclear facilities) are no longer economic to operate. Indeed, these economics have led to the closing of certain “baseload” resources that were no longer able to compete in such a low-priced market, as would be expected in a well-functioning competitive market.

Proposed Federal Coal & Nuclear Subsidies: Criticism

While the energy industry is greatly concerned about grid security and has applauded efforts at both the state and federal level to ensure grid resiliency and to value the longer-term capacity benefits of baseload generation, the industry and industry watchers have provided considerable criticism of the administration’s proposal to provide out-of-market support for coal and nuclear assets.

Vistra’s CEO Curt Morgan had this to say about the DOE’s June 2018 memo justifying the use of the Federal Power Act and Defense Production Act to support failing coal and nuclear facilities:

[Vistra is] against [the solution proposed by the DOE memo] even though we have coal. We think it’s wrong for markets. We understand it’s picking winners and losers. It’s ill conceived. It’s not even touching on the most fundamental national security issue around the energy infrastructure which is transmission. … [I]f you’re going to take something out you want to take out the electric markets and not so much the gas infrastructure. So, the whole premise of the thing is not well-founded, and then the implementation of it, I’ve been thinking about how you do this. I think it’s almost impossible to do this. It’s going to be incredibly messy.[1]

In a statement by PJM[2] regarding the proposal put forth in the DoE memo, they stated:

Markets have helped to establish a reliable grid with historically low prices. Any federal intervention in the market to order customers to buy electricity from specific power plants would be damaging to the markets and therefore costly to consumers. There is no need for any such drastic action… We have acknowledged the concerns raised by officials and regulators about the long-term resilience of the grid and we are embarking on a fuel security initiative that we announced just a few weeks ago. Our goal with that initiative is to ensure that the already reliable electric grid will continue to remain both reliable and resilient for years into the future without the need for government intervention in the marketplace.[3]

In a July 2018 study released by the Brattle Group (commissioned by a cross-section of energy focused interest groups) costs to consumers were estimated to increase $10-35 billion annually over the two-year time horizon envisioned by the memo. In remarks regarding the release of the study, the American Petroleum Institute (one of the commissioners of the study) stated:

[B]ailouts of coal and nuclear plants around the country could raise costs on American consumers and fundamentally hurt the administration’s goal of American energy dominance throughout the world. Affordable, reliable natural gas has earned its share of the electricity markets which is why it has become our nation’s top source of U.S. electricity. The natural gas and oil industry is committed to strengthening national security and is playing a leading role in reducing our decades long dependence on foreign energy but government mandates forcing consumers to buy coal and nuclear power does nothing to advance the security of our nation’s electric grid.

The group Advanced Energy Economy (also a commissioner of the study) stated in remarks related to the study’s release:

Giving aging power plants that are not needed to keep the lights on $34 billion just to exist – that’s money for nothing. It’s too high a price to pay when advanced energy resources and competitive markets can provide the necessary services to keep our grid affordable, reliable, and secure. Independent assessments confirm that these power plants – most of which are decades old – are not needed to ensure reliability or security. We urge the Trump Administration to abandon, and Congress to resist, this exercise in crony capitalism, which comes at the expense of American businesses, families, and economy.

Even the wind industry trade group, American Wind Energy Association (another commissioner of the study), had this to say about the study’s release:

The $10 to $35 billion this policy would take from American taxpayers to keep failing businesses open each year for the next two years is just the down payment – this misguided bailout would also completely upend the competitive electricity markets that are delivering billions in consumer savings. That’s a steep price to pay in an era of U.S. energy abundance, when independent regulators and grid operators agree that orderly power plant retirements do not constitute an emergency.

Market watchers are also confused by the DOE’s approach. Guggenheim Partners, an investing firm, in a June 2018 note to investors stated:

Playing a game of politics: Outside of Texas, New England, and potentially Southern California we do not see any real reliability concerns driving this… We simply do not see any immediate reliability concerns that would warrant a program of this magnitude… which will very likely be highly anti-competitive in several de-regulated markets. NERC’s recent summer assessment highlighted tightness in the ERCOT market and Aliso Canyon-driven concerns in CAISO, but neither of these would require a national solution – especially in TX. PJM, which in our opinion is the genesis for much of the coal retirement-angst inside the beltway and is the largest RTO in the country, has a 23% reserve margin and recently secured adequate capacity through 2022. ISO-NE, which will face its own unique issues in the next few years, has few coal resources the DOE could declare ‘critical’ and only one nuclear unit currently slated to retire (Pilgrim) as Millstone in CT is already on its way to receiving a subsidy for producing carbon free generation and will likely remain a viable operating asset. MISO remains relatively oversupplied with anticipated reserve margins breaching 19% this summer. Finally we highlight that key energy policy stakeholders within DC do not appear to be on the same page as the administration – only 4 weeks ago Senate ENR Chairman Lisa Murkowski told Politico that “we’re not at national emergencies levels.[4]

At the end of the day, policy makers should allow the competitive wholesale markets to work and allow uneconomic assets to retire. The Federal government’s attempt to pick “winners and losers”, without a solid factually driven policy rationale, runs counter to the competitive nature of today’s markets.

[1] Curt Morgan, CEO of Vistra, Analyst Day Remarks, June 12, 2018.

[2] PJM Interconnection coordinates the movement of electricity through all or parts of Delaware, Illinois, Indiana, Kentucky, Maryland, Michigan, New Jersey, North Carolina, Ohio, Pennsylvania, Tennessee, Virginia, West Virginia and the District of Columbia.

[3] PJM Statement on Potential Department of Energy Market Intervention, June 1, 2018 (last accessed 8/23/18)

[4] Pourreza, Shahriar, ”Power and Utilities: Coal/Nuclear: Will Politics ‘Trump’ Reality”, Guggenheim, June 4, 2018, p 1. (emphasis in original)

Proposed Federal Coal & Nuclear Subsidies: Background

Despite these economic realities, there has been an effort at the federal level to provide “support” (i.e., out-of-market subsidies) to uneconomic coal and nuclear generation facilities. The rationale for this support has shifted over time, initially being the need for “fuel secure” resources to ensure grid resiliency and then moving to a national security rationale to protect the grid against disruptions due to natural gas pipeline cybersecurity concerns.

The grid resiliency rationale was outlined in a Notice of Proposed Rulemaking (NOPR) request to the Federal Energy Regulatory Commission (FERC) by Department of Energy Secretary Rick Perry made in September 2017. The NOPR raised the concern that for electric generation that did not have fuel stored on-site (e.g., natural gas facilities fed by pipeline, solar, wind, etc.) any disruption in fuel supply could harm grid resiliency. Therefore, it was necessary to ensure that certain fuel secure resources (namely coal and nuclear) that could store fuel on-site should be subsidized to prevent their departure from the market. In January 2018, the FERC rejected the DOE’s NOPR request and remanded the grid resiliency topic to independent system operators (ISOs).

In March 2018, FirstEnergy Solutions (FES) sent a letter to DOE requesting that DOE explore using the Federal Power Act to support their failing coal and nuclear facilities. This letter came just days after FES announced the intent to close multiple nuclear power plant facilities and just a couple weeks before FES’s declaration of Chapter 11 bankruptcy in April 2018. Subsequently, in April 2018, the White House was reported to be exploring using the Defense Production Act as a justification for supporting ailing coal and nuclear plants. Then a draft DOE memo, leaked in June 2018, outlined the use of both the Federal Power Act and the Defense Production Act as means to provide support to these struggling baseload facilities. The memo outlined a plan to support failing coal and nuclear facilities for a 24-month period to allow time to develop a more permanent solution.

That same month, Energy Secretary Rick Perry and other DOE personnel began to speak publicly about the risk of cyber-attack on U.S. natural gas pipeline infrastructure. While not outlining the immediacy of any cyber-threat to the U.S. pipeline infrastructure, Perry posited that if there was a successful cyber-attack that incapacitated U.S. pipelines and their ability to deliver natural gas to electric generation facilities, it is then a national security imperative to have “fuel secure” resources like coal and nuclear to counterbalance such risk.

Environment

Electricity is an irreplaceable product that is critical to everyday life, whether it be for residences or businesses. We understand and take very seriously our role to provide cost-effective, reliable power to our customers and help fuel the economy. We also understand and take very seriously that our business has an environmental footprint. We have invested billions of dollars to control emissions, to make our existing power plant fleet more efficient, and to advance our generation fleet into newer, more efficient and lower emitting power plants including renewables, batteries, and state-of-the-art, gas-fueled assets. The supply side of our business is experiencing a transition some market-driven and some policy-driven and we must manage our company through this transition in an economic manner. It is not an option to just say no to change. We can and must participate to the long-term benefit of our company and our stakeholders.

Electric Vehicles

Vistra is a member of the Zero Emissions Transportation Association (ZETA), a coalition advocating for 100% electric vehicle sales by 2030. As ZETA will work in Washington to influence policy and ensure market-based approaches are considered in federal legislation around EV infrastructure deployment – not just rate-based/utility solutions.